Christmas and the Taxman

Christmas is traditionally a time of giving – including employers showing gratitude towards staff for a job well done. However, Christmas

parties and gifts can attract the attention of the Taxman.

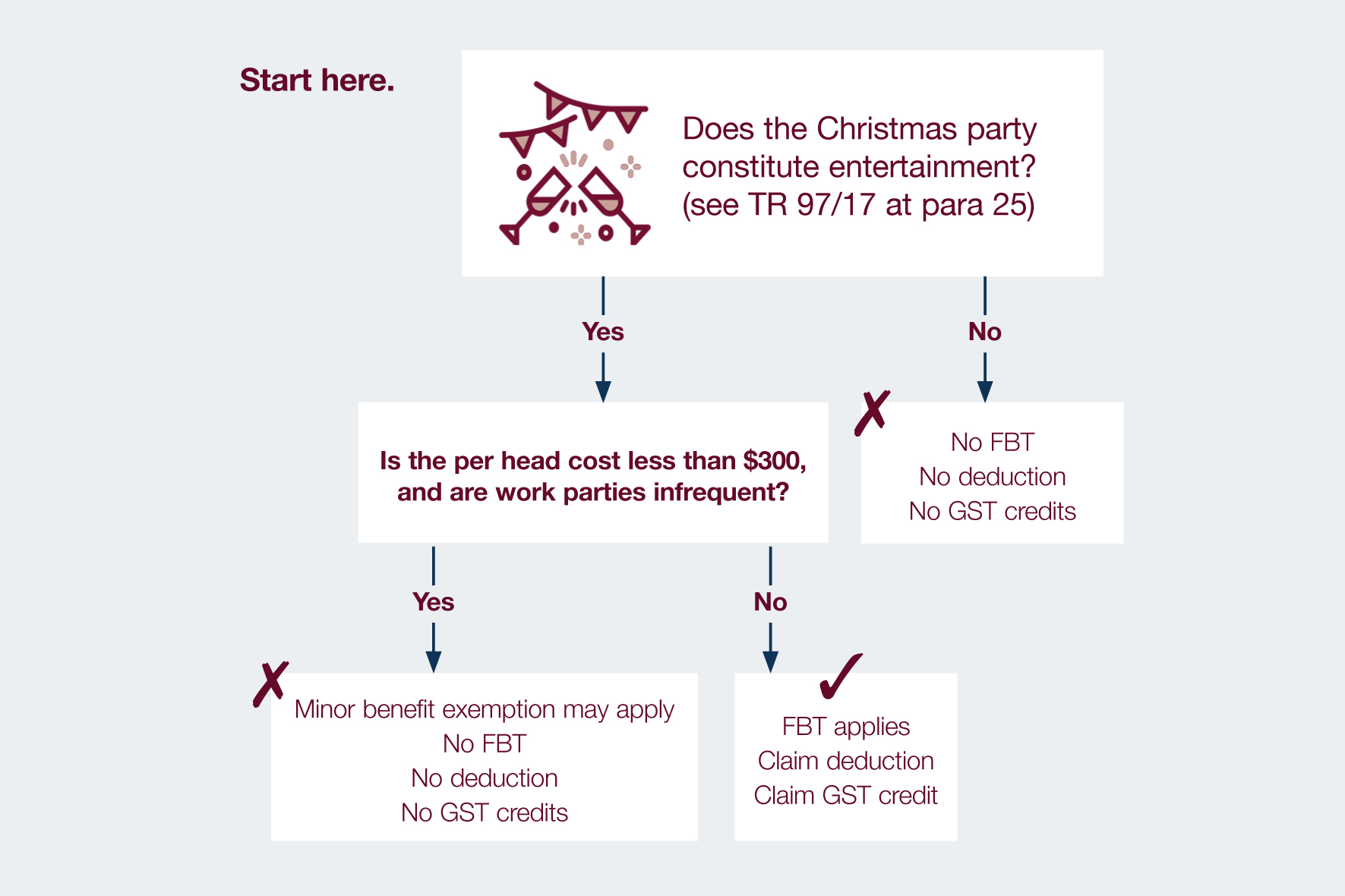

In certain circumstances, an employer can hold a Christmas party for staff and the cost of the party be exempt from Fringe Benefits Tax

(FBT).

Take, for example, an employer who holds a Christmas party at a restaurant for employees and their partners and, apart from perhaps the

Melbourne Cup, it is the only social function they provide for employees each year. Where this is the case, the party is very likely to be

exempt from FBT provided the per-head cost (dinner and drinks) is kept to less than $300 per person. To enjoy this exemption, the employer

must use the “actual method” for valuing FBT meal entertainment.

Using the actual method for valuation

The actual method is the default method for valuing meal entertainment FBT and no election is required to use this method. Under this

method, an employer pays FBT (in the absence of an exemption) on all taxable meal entertainment provided to employees and their associates,

ie, their partners (but not to other parties, such as clients, contractors or suppliers). However, an FBT exemption may apply if the meal

entertainment meets the requirements of the minor benefit exemption. Broadly speaking, under this exemption a benefit will be exempt from

FBT where its value or cost is less than $300 and, if similar or identical benefits are provided during the year, they are only provided on

an infrequent or irregular basis. The less frequent and regular, the more likely each event will be exempt from FBT.

The 50/50 method

This minor benefit exemption is not available if an employer elects to value their meal entertainment under the less-used alternative 50/50

method. Under this method, the employer pays FBT on only 50% of all taxable meal entertainment provided to employees, associates AND

clients, contractors, customers etc. regardless of the cost. Likewise, the employer can only claim a 50% income tax deduction and 50% GST

credits on such meal entertainment.

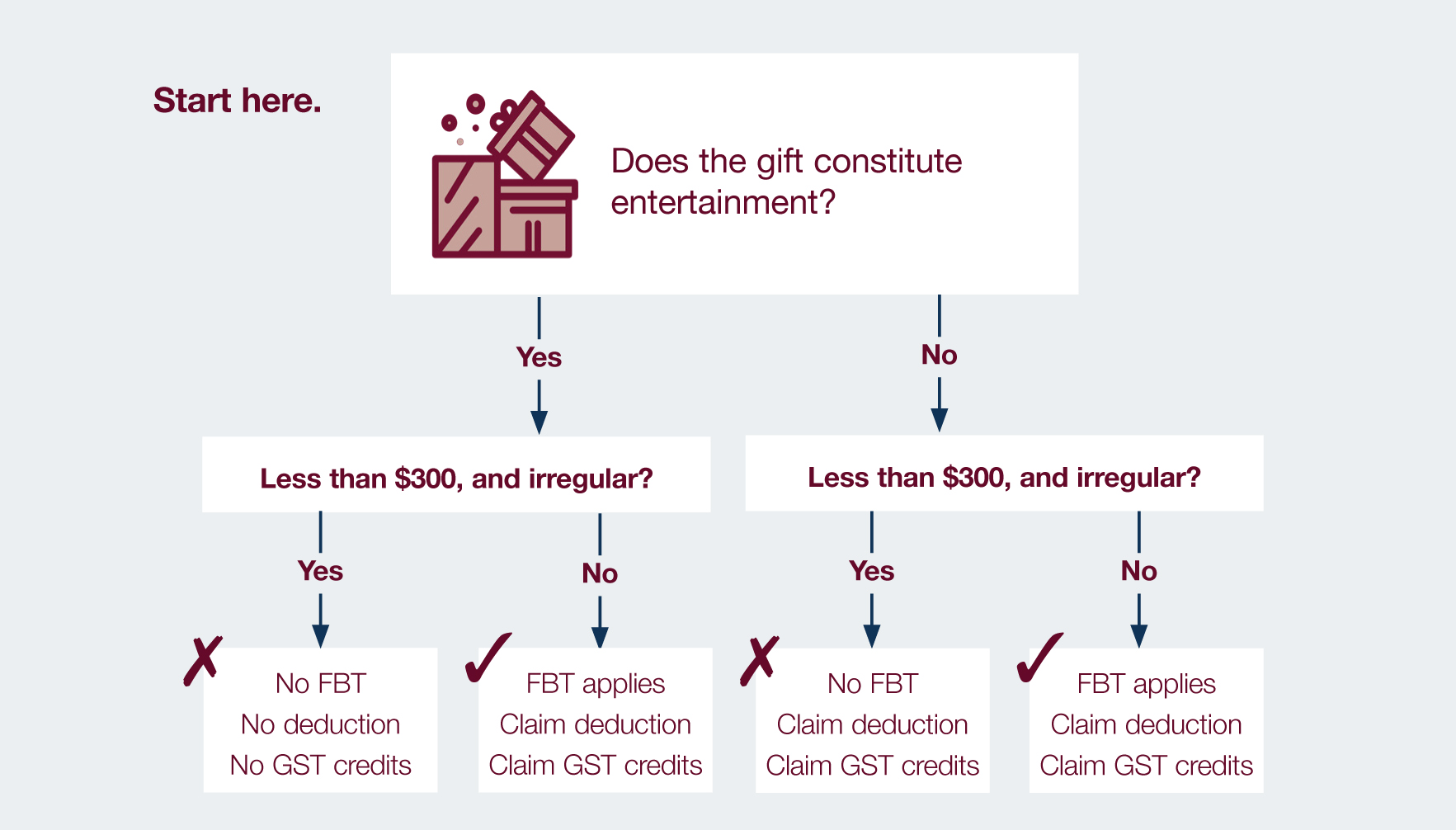

Gifts

If a gift is given at Christmas time and costs less than $300, the minor benefits exemption may be available to exempt from FBT all sorts

of common Christmas gifts to employees. This $300 threshold is separate from the Christmas party meal and entertainment threshold.

Non-entertainment gifts to staff (such as Christmas hampers, bottles of alcohol, gift vouchers, pen sets etc) are tax deductible and

employers can claim GST credits, irrespective of cost. Note, however, that employers can generally avoid paying FBT if they keep the gift

less than $300. If this threshold is exceeded, FBT will apply. Therefore, employers should be conscious of this threshold when providing

such gifts to staff this Christmas.

On the other hand, entertainment gifts to staff (such as tickets to movies/theatre/sporting events, holiday airline tickets etc) that are

less than $300 will generally not attract FBT, are not income tax deductible, and GST credits on it cannot be claimed. If more than $300,

FBT will apply, but a tax deduction and GST credits can be claimed. With the FBT rate at 47%, the tax deduction and GST credits available

are unlikely to provide a better tax outcome than avoiding FBT by keeping the gift to less than $300.

For more details on how to navigate FBT and to understand the most tax-effective way to thank or reward employees, please contact your

Forsyths accountant.

|

The tax treatment of Christmas parties: the actual FBT method |

The tax treatment of gifts |