CGT on sales of property inherited by a foreign resident

Is there CGT when a property inherited from a foreign resident is sold? Am I liable for CGT on a home I inherited from a foreign resident

when I sell it one year later? The following scenario demonstrates how the CGT rules work in this situation.

I have just inherited my uncle’s home. He purchased it on 1 July 1997 and lived in it until 1 July 2012

when he moved to Spain — and where he lived for the last eight years of his life until his death on 1 July 2020. Having inherited the home,

I am now selling it for $1m. The contract of sale will settle on 30 June 2021 (and I have been living in it as my home from the time of his

death and will do so until its sale). Will I be liable for CGT?

The short answer is, yes – and in relation to quite a substantial amount.

By way of background, the rules in s 118-195(1) of the Income Tax Assessment Act 1997 (ITAA 1997) apply to determine in what circumstances

an inherited dwelling can be sold without being subject to CGT.

However, they were amended following the introduction of the measures to deny the CGT main residence exemption to a foreign resident (which

apply, in effect, to sales or disposals occurring after 30 June 2020).

General Rules

The basic exemption rules in s 118- 195 provide that if the dwelling was either a pre-CGT asset of the deceased or the deceased’s main

residence at their date of death (and that was not then being used to produce assessable income), then if the dwelling is sold or otherwise

subject to a relevant CGT event within two years of the deceased’s death, then there will be no CGT on its sale etc.

Note: This two-year period is measured by reference to the settlement date of the contract of sale and it can be extended by the

Commissioner (or an additional 18 months can be self-assessed in accordance with the principles in Practical Compliance Guideline

2019/5).

The rules in s 118-195 also provide that a full CGT exemption is likewise available if the dwelling is subject to a CGT event after it has

been occupied as a main residence, from the time of the deceased’s death until that CGT event, by any of the following persons:

- a surviving spouse, or

- a person who was granted a right to live in it under the will, or

- a beneficiary who inherited the dwelling.

However, if the deceased was an excluded foreign resident just before their death, these full CGT exemption rules do not apply (s

118-195(1)(c)). Note: An excluded foreign resident is a person who has been a foreign resident for a continuous period of more than six

years (s 118-110(4)).

Calculation of Partial Exemption

Where a full CGT main residence exemption does not apply, the partial calculation rules in s 118-200 must be used to calculate the partial

exemption. In the case of a post-CGT dwelling of the deceased, the partial exemption calculation formula in s 118-200(2) requires you to

treat as non-main residence days the following days:

- the days that the deceased owned the dwelling when it was not his or her main residence (s 118-200(a)) — ie, eight years from 1 July 2012 until his death on 1 July 2020, and

- if the deceased was an excluded foreign resident, the “remaining days” in the deceased’s ownership period (s 118-200(2)(aa)) – ie, 15 years from 1 July 1997 until 1 July 2012, and

- the period after the deceased’s death until its sale when it was not the main residence of a surviving spouse, a person with a right to occupy it or a beneficiary (s 118- 200(2)(b)) – ie, nil days in this case because you, as the beneficiary, have lived in it as your main residence in this time.

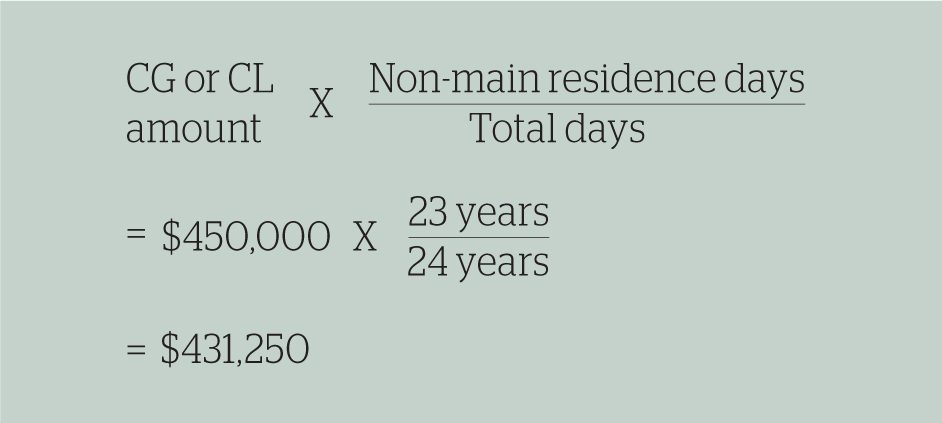

In short, the total non-main residence days in this case where the deceased is an excluded foreign resident at his date of death will be

the deceased’s entire 23-year period of ownership of the dwelling.

The total days of ownership of the dwelling for the purposes of the partial exemption calculation will be from when the deceased acquired

it on 1 July 1997 until its sale by you on 30 June 2021 - being 24 years.

So, if we assume that you make a capital gain on the dwelling of $450,000 (calculated by reference to sale proceeds of $1m), your partial

capital gain calculated under s 118- 200(2) will be:

[Note for simplicity, this calculation is in years instead of days as required.]

However, the CGT 50% discount will be available because the dwelling is treated as having been owned for more than 12 months in this case

(s 115-30(1), Item 4).

(See also Example 1.7 at para 1.43 in Treasury Laws Amendment (Reducing Pressure on Housing Affordability No. 2) Bill 2018, which

introduced the amendments to deny a foreign resident a CGT main residence exemption.)